IRS warns: Deferred payroll taxes due in December

The Internal Revenue Service is sending notices to taxpayers who deferred their Social Security taxes last year, reminding them that half the taxes will be due by the end of this year.

In an email to payroll professionals Friday, the IRS said that it’s sending informational-only CP256V Notices to self-employed individuals and household employers who chose to defer paying some Social Security taxes under the CARES Act in October and November. The notice reminds them that the first installment of deferred Social Security taxes will be due by the end of December and the remainder by the end of next year.

In an email to payroll professionals Friday, the IRS said that it’s sending informational-only CP256V Notices to self-employed individuals and household employers who chose to defer paying some Social Security taxes under the CARES Act in October and November. The notice reminds them that the first installment of deferred Social Security taxes will be due by the end of December and the remainder by the end of next year.

The payroll tax deferral helped taxpayers who found they desperately needed funds to pay their regular expenses during the first year of the pandemic. However, many tax professionals advised their clients that the taxes would eventually come due. The payroll tax relief in the CARES Act for employers differed from the payroll tax holiday that former President Trump issued by executive order in August of last year for employees, which required repayment of the deferred taxes by the end of April 2021. Federal government employees and members of the military were automatically subject to that payroll tax holiday, but most taxpayers and companies avoided opting for it last year, knowing the taxes would eventually have to be paid.

“The CARES Act allowed these types of taxpayers to defer the payment of certain Social Security taxes on their Form 1040 for tax year 2020 over the next two years,” said the IRS. “Half of the deferred Social Security tax is due by Dec. 31, 2021, and the remainder is due by Dec. 31, 2022.”

What you need to do

- Pay your current installment amount by the due date shown on the notice. Note: the notice may not reflect recent payments, but they will still be recorded correctly on your account.

- Review your tax return for the tax period in which you deferred Social Security taxes and subtract any payments you've made. Compare that figure with the amounts shown on your notice. If you discover an error, please contact us at the telephone number shown on the notice.

What you need to know

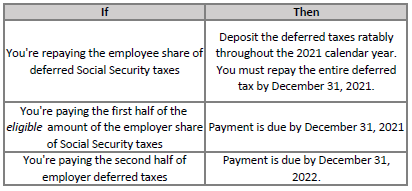

- The first installment amount, due December 31, 2021, is half the employer's share of Social Security taxes you could have deferred (which includes any amount of the employee's share of Social Security taxes deferred under Notice 2020-65, as modified by Notice 2021-11) minus all deposits and payments we've received. For more information, please review Q&A 18 at IRS.gov/etd.

- The second installment, due December 31, 2022, is the remaining unpaid deferred taxes.

Frequently asked questions

Do I have to reply to this notice?

No, this is a courtesy notice for your information only. No response is needed.

How do I make my repayment?

You can make the deferral payments through the Electronic Federal Tax Payment System (EFTPS), by credit or debit card, or with a check or money order. Note: you must make these payments separate from other tax payments to ensure they're applied to the deferred payroll tax balance. IRS systems won't recognize the payment if it's with other tax payments or sent as a deposit.

To make the deferred payment using EFTPS, select deferral payment and change the date to the applicable tax period for the payment.

If the employee no longer works for the organization, you must repay the entire deferred amount of the employee's portion of Social Security tax then collect the employee's portion using your own recovery methods.

How do I make a payment for a deferred amount on an aggregate return?

Third-party payers (such as an Internal Revenue Code Section 3504 agent, a certified professional employer organization, a non-certified professional employer organization, or other agents designated with Form 2678, Employer/Payer Appointment of Agent) file aggregate returns to show the employer's deferred tax.

Employers should coordinate with their third-party payer to pay deferred taxes owed by the December 31, 2021, and December 31, 2022, due dates. This helps ensure the third party properly records the payment and the correct employer identification number (EIN) and tax period are noted with the payment so the IRS can apply it properly.

Employers should continue coordinating with their third-party payer to ensure payments are applied under the third party's EIN (unless the employer receives an IRS notification stating the unpaid deferral amount has been moved to their EIN).

What if I cannot pay my deferred taxes?

You may be eligible for a payment plan or other payment options. Note: if the IRS doesn’t receive your payment by the applicable due dates, the deferred taxes may be subject to Failure to Deposit penalties.

When should I repay deferred taxes?

The following table shows the schedule for repayment:

Penalties and interest begin accruing on the day payments are due if they aren't timely paid.

How do third-party payers report unpaid deferred amounts from aggregate returns?

Employers are solely responsible for payment of the deferred taxes they requested for any wages paid by the third-party payer. If the third-party payer filed an aggregate return and receives a balance due notice for the employer's unpaid portion of deferred Social Security tax, the third-party may notify the IRS by eFaxing the following information with a coversheet to 844-255-1856:

- Copy of the Schedule R (Form 941 or 943) for relevant tax periods

- Client (common law employer) name, EIN, and current address

- Total deferred amount per tax period

- Unpaid part of the deferred amount, per tax period

- List of deferral payments by client or by the third-party payer on behalf of client(dates and amounts), per tax period

- If applicable, date client separated from aggregate filer

Year-End Individual Tax Planning

It is getting to be that time of year to review your tax situation and explore options to minimize your tax bill.

Due to the enactment of legislation to offset the economic burden wrought by COVID-19, there is a lot to consider when reviewing year-end tax planning options. Pandemic-related tax breaks include an expanded dependent care assistance, payroll tax credits for self-employed individuals, substantial increases in the child tax credit and the earned income tax credit, $1,400 recovery rebates for many taxpayers, and an exclusion from income for certain student loan forgiveness, to name just a few.

Due to the enactment of legislation to offset the economic burden wrought by COVID-19, there is a lot to consider when reviewing year-end tax planning options. Pandemic-related tax breaks include an expanded dependent care assistance, payroll tax credits for self-employed individuals, substantial increases in the child tax credit and the earned income tax credit, $1,400 recovery rebates for many taxpayers, and an exclusion from income for certain student loan forgiveness, to name just a few.

Presently, Congress is engaged in negotiations on a tax and spending bill that would likely result in major tax changes beginning next year. Should such a bill pass, we will want to factor such changes into our year-end planning. For now, we'll need to base our planning on existing law.

The following are some of the considerations we should explore when discussing the tax breaks from which you may benefit, as well as the strategies we can employ to help minimize your taxable income and resulting federal tax liability.

2021 Recovery Rebate

Under American Rescue Plan (ARP) Act, passed in March, individuals with income under a certain level are entitled to a recovery rebate tax credit. These are direct payments (sometimes referred to as "stimulus checks") to individuals by the government.

Single individuals and joint filers are entitled to a payment of $1,400 for each eligible individual. An eligible individual is any individual other than (1) a nonresident alien, (2) a dependent of another taxpayer, and (3) an estate or trust. For these purposes, the term "dependent" includes not just children but qualifying relatives. The amount of the recovery rebate phases out for income over a certain level. The 2021 recovery rebate began phasing out starting at $75,000 of adjusted gross income (AGI) for an individual ($112,500 for heads of household and $150,000 in the case of a joint return or surviving spouse) and was completely phased out where an individual's AGI is $80,000 ($120,000 for heads of household and $160,000 in the case of a joint return or surviving spouse).

The government began issuing the rebates based on 2019 income tax returns, or 2020 returns for individuals who filed their 2020 returns in time. The calculation for the correct amount of the rebate will be part of your 2021 tax return. If your 2021 tax return indicates a rebate larger than your stimulus check (because, for example, your income went down or you had another child), any additional amount will be claimed as a credit against your 2021 tax bill. On the flip side, if the 2021 rebate calculation shows an amount in excess of what you were entitled to, you do not have to repay that excess.

Filing Status

Your tax return filing status can impact the amount of taxes you pay. For example, if you qualify for head-of-household (HOH) filing status, you are entitled to a higher standard deduction and more favorable tax rates. To qualify as HOH, you must be unmarried or considered unmarried (i.e., legally separated or living apart from a spouse) and provide a home for certain other persons. If you are in such a situation, we need to review whether you qualify for HOH filing status.

If you are married, you'll either be filing your return using the married filing jointly or married filing separately filing status. Generally, married filing separately is not beneficial for tax purposes, but in some unique cases, such as when one party earns substantially less or when one party may be subject to IRS penalties for issues relating to tax reporting, it may be advantageous to file as married filing separately. Additionally, if one spouse was not a full-year U.S. resident, an election is available to file a joint tax return where such joint filing status would otherwise not apply and this may help reduce a couple's tax liability.

Income, Deductions, and Credits

Standard Deduction versus Itemized Deductions. The Tax Cuts and Jobs Act of 2017 (TCJA) substantially increased the standard deduction amounts, thus making itemized deductions less attractive for many individuals. For 2021, the standard deduction amounts are: $12,550 (single); $18,800 (head of household); $25,100 (married filing jointly); and $12,550 (married filing separately). An additional standard deduction amount of $1,350 applies for taxpayers who are 65 or older or blind. This additional amount is increased to $1,700 if the individual is also unmarried and not a surviving spouse. If the taxpayer is 65 or older and blind, the deduction is doubled.

If the total of your itemized deductions in 2021 will be close to your standard deduction amount, we should evaluate whether alternating between bunching itemized deductions into 2021 and taking the standard deduction in 2022 (or vice versa) could provide a net-tax benefit over the two-year period. For example, you might consider doubling up this year on your charitable contributions rather than spreading the contributions over a two-year period. If these contributions, along with your mortgage interest, medical expenses (discussed below), and state income and property taxes (subject to the $10,000 deduction limitation on such taxes that applies to both single individuals and married couples filing jointly; and the $5,000 limitation on such expenses for married filing separately returns), exceed your standard deduction, then itemizing such expenses this year and taking the standard deduction next year may be appropriate.

Medical Expenses, Health Savings Accounts, and Flexible Savings Accounts. As a result of the COVID-19 pandemic, a number of individuals have incurred more medical expenses than usual. For 2021, our-of-pocket medical expenses you have paid in 2021 are deductible as an itemized deduction to the extent they exceed 7.5 percent of your adjusted gross income. To be deductible, medical care expenses must be primarily to alleviate or prevent a physical or mental disability or illness. They don't include expenses that are merely beneficial to general health, such as vitamins or a vacation. Deductible expenses include not only hospitalization expenses, but also health insurance premiums and the amounts you pay for transportation to get medical care. Medical expenses also include amounts paid for qualified long-term care services and limited amounts paid for any qualified long-term care insurance contract. Depending on what your taxable income is expected to be in 2021 and 2022, and whether itemizing deductions would be advantageous for you in either year, you may want to accelerate any optional medical expenses into 2021 or defer them until 2022. The right approach depends on your income for each year, expected medical expenses, as well as your other itemized deductions.

Medical Expenses, Health Savings Accounts, and Flexible Savings Accounts. As a result of the COVID-19 pandemic, a number of individuals have incurred more medical expenses than usual. For 2021, our-of-pocket medical expenses you have paid in 2021 are deductible as an itemized deduction to the extent they exceed 7.5 percent of your adjusted gross income. To be deductible, medical care expenses must be primarily to alleviate or prevent a physical or mental disability or illness. They don't include expenses that are merely beneficial to general health, such as vitamins or a vacation. Deductible expenses include not only hospitalization expenses, but also health insurance premiums and the amounts you pay for transportation to get medical care. Medical expenses also include amounts paid for qualified long-term care services and limited amounts paid for any qualified long-term care insurance contract. Depending on what your taxable income is expected to be in 2021 and 2022, and whether itemizing deductions would be advantageous for you in either year, you may want to accelerate any optional medical expenses into 2021 or defer them until 2022. The right approach depends on your income for each year, expected medical expenses, as well as your other itemized deductions.

You may also want to consider health saving accounts (HSAs) if you don't already have one. These are tax-advantaged accounts which help individuals who have high-deductible health plans. If you are eligible to set up such an account, you can deduct the amount you contribute to the account in computing adjusted gross income. These contributions are deductible whether you itemize deductions or not. Distributions from an HSA are tax free to the extent they are used to pay for qualified medical expenses (i.e., medical, dental, and vision expenses). For 2021, the annual contribution limits are $3,600 for an individual with self-only coverage and $7,200 for an individual with family coverage.

In addition, if you are not already doing so and your employer offers a Flexible Spending Account (FSA), consider setting aside some of your earnings tax free in such an account so you can pay medical and dental bills with pre-tax money. The maximum amount that the IRS will allow to be set aside for 2021 limit is $2,750. Since you don't pay taxes on this money, you'll save an amount equal to the taxes you would have paid on the money you set aside. FSA funds can be used to pay deductibles and co-payments, but not for insurance premiums. You can also spend FSA funds on prescription medications, as well as over-the-counter medicines, generally with a doctor's prescription. Reimbursements for insulin are allowed without a prescription. Finally, FSAs may also be used to cover costs of medical equipment like crutches, supplies like bandages, and diagnostic devices like blood sugar test kits.

Charitable Contributions. While the tax benefits of making charitable contributions and taking an itemized deduction for such contributions were tamped down as a result of the increases made to the standard deduction amounts, a law passed at the end of 2020 modified the charitable contribution rules for 2021 tax returns. As a result, eligible individuals can claim an above-the-line deduction of up to $300 ($600 in the case of a joint return) for qualified charitable contributions made during 2021. An eligible individual is an individual who does not elect to itemize deductions. Thus, absent this provision, anyone taking the standard deduction would be ineligible to take a charitable contribution deduction. A qualified charitable contribution is a cash contribution paid in 2021 to an eligible charitable organization. Contributions of non-cash property, such as securities, are not qualified contributions.

Charitable Contributions. While the tax benefits of making charitable contributions and taking an itemized deduction for such contributions were tamped down as a result of the increases made to the standard deduction amounts, a law passed at the end of 2020 modified the charitable contribution rules for 2021 tax returns. As a result, eligible individuals can claim an above-the-line deduction of up to $300 ($600 in the case of a joint return) for qualified charitable contributions made during 2021. An eligible individual is an individual who does not elect to itemize deductions. Thus, absent this provision, anyone taking the standard deduction would be ineligible to take a charitable contribution deduction. A qualified charitable contribution is a cash contribution paid in 2021 to an eligible charitable organization. Contributions of non-cash property, such as securities, are not qualified contributions.

In addition, if you are itemizing your deductions and have substantial charitable contributions, the new rules modified the percentage limitation rules that could otherwise limit your charitable contribution deduction. As a result, for charitable contributions made during 2021, any qualified contribution is allowed as a deduction to the extent that the aggregate of such contributions does not exceed the excess of your charitable contribution base over the amount of all other charitable contributions. Excess contributions are eligible for a five-year carryover.

As in prior years, you can reap a larger tax benefit by donating appreciated assets, such as stock, to a charity. Generally, the higher the appreciated value of an asset, the bigger the potential value of the tax benefit. Donating appreciated assets not only entitles you to a charitable contribution deduction but also helps you avoid the capital gains tax that would otherwise be due if you sold your stock. For example, if you own stock with a fair market value of $1,000 that was purchased for $250 and your capital gains tax rate is 15 percent, the capital gains tax you would owe if you sold that stock is $113 ($750 gain x 15%). If you donate that stock instead of selling it, and are in the 24 percent tax bracket, your ordinary income deduction is worth $240 ($1,000 FMV x 24% tax rate). You also save the $113 in capital gains tax that you would otherwise pay if you sold the stock; that amount goes to the charity. Thus, the after-tax cost of the gift of appreciated stock is $647 ($1,000 - $240 - $113) compared to the after-tax cost of a donation of $1,000 cash which would be $760 ($1,000 - $240). However, it's important to also keep in mind that tax deductions for contributions of appreciated long-term capital gain property may be limited to a certain percentage of your adjusted gross income depending on the amount of the deduction.

Finally, if you have an individual retirement account and are 70 1/2 years old and older, you are eligible to make a charitable contribution directly from your IRA. This is more advantageous than taking a distribution and making a donation to the charity that may or may not be deductible as an itemized deduction. If your itemized deductions, including the contribution, are less than your standard deduction, then you receive no tax benefit from taking a taxable distribution and donating that distribution. By making the donation directly from your IRA to a charity, you eliminate having the IRA distribution included in your income. This in turn reduces your adjusted gross income (AGI). Because various tax-related items, such as the medical expense deduction or the taxability of social security income or the 3.8 percent net investment income tax, are calculated based on your AGI, a reduced AGI can potentially increase your medical expense deduction, reduce the tax on social security income, and reduce any net investment income tax.

Expenses Incurred While Working from Home. Although more people have been working from home this year due to the pandemic, related expenses are not deductible if you are an employee. However, if you are self-employed and worked from home during the year, tax deductions are still available. Thus, if you have been working from home as an independent contractor, we should discuss what expenses you have incurred that might offset that taxable income.

Mortgage Interest Deduction. If you sold your principal residence during the year and acquired a new principal residence, the deduction for any interest on your acquisition indebtedness (i.e., your mortgage) could be limited. The interest deduction on mortgages of more than $750,000 obtained after December 14, 2017, is limited to the portion of the interest allocable to $750,000 ($375,000 in the case of married taxpayers filing separately). If you have a mortgage on a principle residence acquired before December 15, 2017, the mortgage interest limitation applies to mortgages of $1,000,000 ($500,000 in the case of married taxpayers filing separately) or less. However, if you operate a business from your home, an allocable portion of your mortgage interest is not subject to these limitations.

Interest on Home Equity Indebtedness. You can potentially deduct interest paid on home equity indebtedness, but only if you used the debt to buy, build, or substantially improve your home. Thus, for example, interest on a home equity loan used to build an addition to your existing home is typically deductible, while interest on the same loan used to pay personal expenses, such as credit card debt, is not.

Sale of a Home. If you sold your home this year, up to $250,000 ($500,000 for married filing jointly) of the gain on the sale is excludible from income. However, this amount is reduced if part of your home was rented out or used for business purposes. Generally, a loss on the sale of a home is not deductible. But again, if you rented part of your home or otherwise used it for business, the loss attributable to that portion of the home is deductible.

Discharge of Qualified Principal Residence Indebtedness. If you had any qualified principal residence indebtedness which was discharged in 2021, it is not includible in gross income.

Deductions for Mortgage Insurance Premiums. You may be entitled to treat amounts paid during the year for any qualified mortgage insurance as deductible qualified residence interest if the insurance was obtained in connection with acquisition debt for a qualified residence.

Deductions for Excess Business Losses. The ARP allows taxpayers other than corporations to deduct excess farm losses and excess business losses through 2027. An excess business loss for the tax year is the excess of aggregate deductions attributable to your trades or businesses over the sum of your aggregate gross income or gain plus a threshold amount. The threshold amount for 2021 is $262,000 or $524,000 for joint returns.

Qualified Business Income Passthrough Tax Break. Under the qualified business income tax break, a 20 percent deduction is allowed for qualified business income from sole proprietorships, S corporations, partnerships, and LLCs taxed as partnerships. If you qualify for the deduction, which is available to both itemizers and nonitemizers, it is taken on your individual tax return as a reduction to taxable income. This tax break is subject to some complicated restrictions and limitations, but the rules that apply to individuals with taxable income at or below $164,900 ($329,800 for joint filers; $164,925 for married individuals filing separately) are simpler and more permissive than the ones that apply to individuals with taxable income above those thresholds.

Child Tax Credit. The ARP significantly increased the child tax credit (CTC) available in 2021. The CTC was increased from $2,000 to $3,000 or, for children under 6, to $3,600. The age of a child for which the credit is available was raised from 16 to 17. Further, the refundable amount of the 2021 CTC equals the entire credit amount, rather being based on an earned income formula. Under modified phase-out rules, the modified adjusted gross income threshold which determines if an individual qualifies for the CTC was reduced to $150,000 in the case of a joint return or surviving spouse, $112,500 in the case of a head of household, and $75,000 in any other case. This special phase-out reduction is limited to the lesser of the applicable credit increase amount (i.e., either $1,000 or $1,600) or 5 percent of the applicable phase-out threshold range.

Taxpayers with refundable child tax credits may be eligible to receive advance payments of the credit.

Earned Income Credit. The ARP also expanded eligibility for the earned income tax credit (EITC) in 2021 and increased the amount of the credit available. For 2021, the minimum age to claim the so-called "childless EITC" for workers without qualifying children (i.e., dependent children who live with the taxpayer for more than half the year) is reduced from 25 to 19 (except for certain full-time students) and the upper age limit for the childless EITC is eliminated. In addition, the childless EITC amount has been increased so that the maximum EITC for 2021 for a childless individual is now $1,502.

The ARP also repealed a provision which prohibited an otherwise EITC-eligible taxpayer with qualifying children from claiming the childless EITC if he or she could not claim the EITC with respect to qualifying children due to failure to meet child identification requirements (including a valid SSN for qualifying children). This prohibition no longer applies.

Finally, the ARP increased to $10,000 the amount of investment income a person could have and still qualify for the EITC. In addition, taxpayers can compute their EITC amount for 2021 by substituting their 2019 earned income for their 2021 earned income, if 2021 earned income is less than 2019 earned income.

Dependent Care Assistance Tax Benefits. The ARP provided a number of favorable changes to tax benefits relating to dependent care assistance, including: (1) making the child and dependent care tax credit (CDCTC) refundable; (2) increasing the amount of expenses eligible for the CDCTC; (3) increasing the maximum rate of the CDCTC; (4) increasing the applicable percentage of expenses eligible for the CDCTC; and (5) increasing the exclusion from income for employer-provided dependent care assistance.

Generally, you may be eligible for a nonrefundable CDCTC for up to 35 percent of the expenses paid to someone to care for your child or your dependent so that you can work or look for work. For 2021, the dependent care credit is refundable for an individual who lives in the United States for more than one-half of the tax year. Under the ARP, the amount of child and dependent care expenses that are eligible for the credit was increased to $8,000 for one qualifying individual and $16,000 for two or more qualifying individuals. The maximum credit rate also goes up from 35 to 50 percent and a phaseout thresholds begin at $125,000 of adjusted gross income (i.e., household income). At $125,000, the credit percentage begins to phase out, and plateaus at 20 percent. This 20-percent credit rate phases out for taxpayers whose adjusted gross income is in excess of $400,000. In addition, the amount of employer-provided dependent care assistance that may be excluded from income has been increased from $5,000 to $10,500 (from $2,500 to $5,250 in the case of a separate return filed by a married individual) for 2021.

Premium Tax Credit. A health insurance subsidy is available through a premium assistance credit for eligible individuals and families who purchase health insurance through insurance Exchanges offered under the Patient Protection and Affordable Care Act (PPACA). The premium assistance credit is refundable and payable in advance directly to the insurer on the Exchange. Individuals with incomes exceeding 400 percent of the poverty level are normally not eligible for these subsidies. However, the ARP eliminated that provision for tax years beginning in 2021 or 2022 and allows anyone to qualify for the subsidy. In addition, the provision limits the percentage of a person's income paid for health insurance under a PPACA plan to 8.5 percent of income.

Education-Related Deductions and Credits. Certain education-related tax deductions, credits, and exclusions from income may apply for 2021. Tax-free distributions from a qualified tuition program, also referred to as a Section 529 plan, of up to $10,000 are allowed for qualified higher education expenses. Qualified higher education expenses for this purpose include tuition expenses in connection with a designated beneficiary's enrollment or attendance at an elementary or secondary public, private, or religious school, i.e., kindergarten through grade 12. It also includes expenses for fees, books, supplies, and equipment required for the participation in certain apprenticeship programs and qualified education loan repayments in limited amounts. A special rule allows tax-free distributions to a sibling of a designated beneficiary (i.e., a brother, sister, stepbrother, or stepsister). As a result, a 529 account holder can make a student loan distribution to a sibling of the designated beneficiary without changing the designated beneficiary of the account.

Education-Related Deductions and Credits. Certain education-related tax deductions, credits, and exclusions from income may apply for 2021. Tax-free distributions from a qualified tuition program, also referred to as a Section 529 plan, of up to $10,000 are allowed for qualified higher education expenses. Qualified higher education expenses for this purpose include tuition expenses in connection with a designated beneficiary's enrollment or attendance at an elementary or secondary public, private, or religious school, i.e., kindergarten through grade 12. It also includes expenses for fees, books, supplies, and equipment required for the participation in certain apprenticeship programs and qualified education loan repayments in limited amounts. A special rule allows tax-free distributions to a sibling of a designated beneficiary (i.e., a brother, sister, stepbrother, or stepsister). As a result, a 529 account holder can make a student loan distribution to a sibling of the designated beneficiary without changing the designated beneficiary of the account.

In addition, if your modified adjusted gross income level is below certain thresholds, the following are also available for 2021: an American Opportunity Tax Credit of up to $2,500 per year for each eligible student; a Lifetime Learning credit of up to $2,000 for tuition and fees paid for the enrollment or attendance of yourself, your spouse, or your dependents for courses of instruction at an eligible educational institution; an exclusion from income for education savings bond interest received; and a deduction from gross income for student loan interest of up to $2,500. In addition, under the ARP, certain discharges of students loans occurring in years 2021 through 2025 are excludible from income.

Credit for Sick Leave for Self-Employed Individuals. As a result of the COVID-19 pandemic, special income tax credits were enacted for self-employed individuals. If you are considered an eligible self-employed individual, you may qualify for an income tax credit for a qualified sick leave equivalent amount. You are an eligible self-employed individual if you regularly carry on any trade or business and would be entitled to receive paid leave during the tax year under the Emergency Paid Sick Leave Act added by the Families First Act. The calculation of the qualified sick leave equivalent amount is quite complicated but is generally equal to the number of days during the tax year that you could not perform services for which you would have been entitled to sick leave, multiplied by the lesser of two amounts: (1) $511, or (2) 100 percent of your average daily self-employment income. The number of days taken into account in determining the qualified sick leave equivalent amount may not generally exceed 10 days. Your average daily self-employment income under this provision is an amount equal to the net earnings from self-employment for the year divided by 260. In addition, if you have appropriate documentation, the credit is refundable.

Credit for Family Leave for Certain Self-Employed Individuals. Another coronavirus-related income tax credit that may be available to you is a credit for a qualified family leave equivalent amount with respect to wages paid before October 1, 2021. The qualified family leave equivalent amount is an amount equal to the number of days (up to 50) during the tax year that you could not perform services for which you would be entitled, if you were employed by an employer, to paid leave under the Emergency Family and Medical Leave Expansion Act, multiplied by the lesser of two amounts: (1) 67 percent of your average daily self-employment income for the tax year, or (2) $200. Your average daily self-employment income under the provision is an amount equal to your net earnings from self-employment for the year divided by 260. This credit is also refundable.

Retirement Planning

If you can afford to do so, investing the maximum amount allowable in a qualified retirement plan will yield a large tax benefit. If your employer has a 401(k) plan and you are under age 50, you can defer up to $19,500 of income into that plan for 2021. Catch-up contributions of $6,500 are allowed if you are 50 or over. If you have a SIMPLE 401(k), the maximum pre-tax contribution for 2021 is $13,500. That amount increases to $16,500 if you are 50 or older. The maximum IRA deductible contribution for 2021 is $6,000 and that amount increases to $7,000 if you are 50 or over.

Life Events

Life Events

Life events can have a significant impact on your tax liability. For example, if your filing status last year was Head of Household or Surviving Spouse and your filing status for 2021 is Single, then your tax rate will go up. If you married or divorced during the year and changed your name, you need to notify the Social Security Administration (SSA). Similarly, the SSA should be notified if you have a dependent whose name has been changed. A mismatch between the name shown on the tax return and the SSA records can cause problems in the processing of tax returns and may even delay tax refunds. If you have been impacted by a life event, such as a birth or death in your family, the loss of a job or a change in jobs, or if you retired during the year, all of these can affect your tax situation.

Conclusion

Please call at your convenience so we can set up an appointment to discuss your 2021 tax return and determine if any estimated tax payment may be due before year end.

How Biden's Build Back Better Plan Would Tax the Rich

Key Points:

-

President Joe Biden issued a $1.75 trillion social and climate spending plan on Thursday. About $1 trillion would be financed by higher taxes on wealthy Americans.

-

The Build Back Better proposal would levy a tax surcharge on Americans who earn more than $10 million, invest in more IRS enforcement and raise taxes for some business owners.

-

It’s unclear whether the plan has the full backing of Democrats in the House and Senate.

Thursdays big news was the release of a $1.75 trillion social and climate spending bill. More than half of the bill would be financed by tax reform aimed at wealthy Americans.

Millionaire and billionaire surtax

Millionaire and billionaire surtax

A 5% surtax rate on income more than $10 million and and additional 3% surtax rate on income above $25 million would be in effect. This surtax is estimated to raise $230 billion over the next 10 years and would go into effect for tax years beginning January 1, 2022. As of 2018, there were 22,112 tax returns reporting income of more than $10 million.

“I don’t want to punish anyone’s success; I’m a capitalist,” President Biden said in a speech Thursday. “All I’m asking is, pay your fair share.” He also reiterated that households earning less than $400,000 per year wouldn’t “have to pay a penny more” in federal taxes, and would likely get a tax cut from the proposal via the enhanced child tax credit. The top 1% evade more than $160 billion per year in taxes, according to the White House.

Although specifics are omitted, the bill seems to have abandoned many of the tax proposals made last month by the House Ways and Means Committee. For example, the framework doesn’t raise the top income tax rate or top rate on investment income (with exception to those subject to the proposed surtax). It also doesn’t impose required distributions from large retirement account or alter rules around estate and trust taxes.

Business income

There are two provisions in the Build Back Better framework related to business income.

One would apply a 3.8% Medicare surtax to all income from pass-through businesses and another would limit a tax break on business losses for the wealthy.

The reforms would raise $250 billion and $170 billion, respectively, over a decade, according to estimates.

Currently, the owners of most pass-through businesses are subject to a 3.8% self-employment tax or net investment income tax. (Such businesses, like sole proprietorships and partnerships, pass their earnings to owners’ individual tax returns.)

However, some profits (namely, those of S corporations) aren’t subject to the 3.8% net investment income tax, which was created by the Affordable Care Act to fund Medicare expansion. The proposal would close this loophole for wealthy business owners.

It would apply to single taxpayers with more than $400,000 in taxable income or married couples filing a joint return with more than $500,000 in taxable income.

The second proposal is also somewhat vague on business losses. But the House tax proposal last month, which contained a similar measure, may offer a clue; it would permanently disallow excess business losses (meaning, net tax deductions that exceed their business income).

This applies to businesses that aren’t structured as a corporation.

Both provisions would kick in after Dec. 31.

IRS enforcement

Democrats’ plan would give $79 billion in new funding to the IRS to help close the so-called tax gap.

Relative to other taxpayers, they get a bigger share of income from opaque sources, such as certain business arrangements that aren’t as readily subject to tax reporting or withholding, according to Watson.

The IRS would hire enforcement agents trained to pursue wealthy tax evaders, overhaul 1960s-era technology and invest in taxpayer services to help ordinary Americans, according to the White House.

It estimates these measures would raise $400 billion over 10 years — the single-biggest revenue raiser in the proposal.

However, some question how lawmakers arrived at that revenue figure. The Treasury Department estimated last month that an $80 billion IRS investment would generate $320 billion in revenue over a decade.